Another small step out of austerity – before a giant leap into the unknown

15 March 2019This blog post summaries the content of the Spring Statement (2019) Briefing produced by Guto Ifan and Cian Sion of the Wales Fiscal Analysis team.

Amidst the political drama of crucial Brexit votes this week, the Chancellor of the Exchequer delivered his Spring Statement on the UK’s economy and public finances. Usually the big news story of the day, this (semi) fiscal event scarcely made it into the top ten headlines. In this blog post, we look at what the Spring Statement and forecasts from the Office for Budget Responsibility (OBR) can tell us about future Welsh budgets and Welsh public services.

OBR forecasts and the UK economy

Uncertainty surrounding Brexit and a slowing world economy has meant that real UK GDP growth in 2019 has been revised downwards from 1.6 to 1.2 per cent. The UK economy is now forecast to be 2.7% smaller at the end of 2020 than what was forecast in March 2016.

However, defying anaemic economic growth, the public finances have continued to improve and outperform expectations.

On the spending side, forecast interest payments on the national debt were £3.6 billion a year lower than what had been projected in October, reflecting lower interest rates and inflation.

Meanwhile, the forecast for tax receipts was revised upwards by £3.5 billion a year on average. A nearly 6% growth in the incomes of the top 0.1 per cent has provided a welcome boost to this total. It does, however, signal a worrying increase in income inequality.

It is forecast that the structural deficit (the difference between government revenue and expenditure) will comfortably meet the Government’s ‘fiscal mandate’, which requires public borrowing to be no more than 2 per cent of GDP by 2020-21. [1]

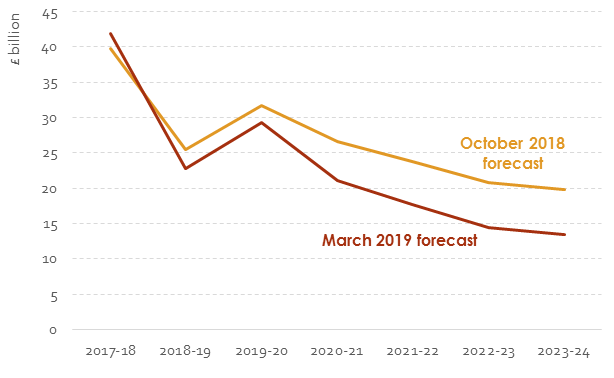

Figure 1: Public sector net borrowing over forecast period

Source: HM Treasury (2018 and previous) Public Expenditure Statistical Analyses; OBR (2019) Economic and Fiscal Outlook March 2019; and authors’ calculations

Given the size of this fiscal ‘headroom’, spending on public services could be increased by around £15 billion a year, and the Chancellor would still fulfil his fiscal mandate on current forecasts.

Despite this, no significant new spending decisions were made at this Spring Statement. In contrast to last October, the windfall from better-than-expected public finances was banked rather than spent.

The Spending Review and future Welsh budgets

The UK Government has already committed an extra £20.5 billion a year to the NHS in England by 2023-24. Given existing commitments on defence and international aid, the path for over half of day-to-day spending has already been decided.

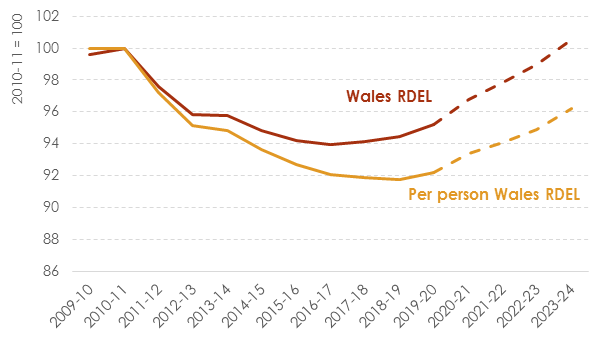

Figure 2 projects what current plans would mean for the path of the Welsh block grant for day-to-day spending to 2023-24, assuming increases in spending on unprotected areas are spread evenly across other UK government departments.

Figure 2: Welsh block grant for day-to-day spending (Wales resource DEL excluding depreciation, 2010-11 = 100)

Source: HM Treasury (2018 and previous) Public Expenditure Statistical Analyses; OBR (2019) Economic and Fiscal Outlook March 2019; and authors’ calculations [2]

Under these projections, the amount available to the Welsh Government for day-to-day spending would grow by approximately 1.3% a year over the Spending Review period. This increase in spending would mean that the Welsh Government’s day-to-day spending reaches its 2010-11 level in real terms by 2023-24 (red line). On a per person basis however, it will remain well below its 2010-11 level (yellow line).

Brexit uncertainty

UK legislation mandates that the OBR base its economic and fiscal forecasts on current government policy. This means that the most recent forecasts are underpinned by the assumption that the UK will leave the European Union on 29 March 2019 and enter a transition period until December 2020

Of course, it is still far from certain that there will be an orderly withdrawal from the EU. Moreover, it is now almost unforeseeable that the UK will enter a transition period on 29 March as OBR forecasts assume. If the UK Parliament fails to ratify the Withdrawal Agreement and Article 50 is not extended nor revoked prior to the March deadline, the UK leaves the EU with no deal by default.

The Chancellor used the Spring Statement to reiterate that a no deal Brexit would mean ‘significant disruption in the short and medium-term’ and a ‘smaller, less prosperous economy in the long-term’. He will hope that his promised mix of increased public spending, tax cuts and investment persuades MPs to back the government’s Withdrawal Agreement (potentially at a third vote).

Devolved tax revenue forecasts

From April 2019, a newly-devolved Welsh Rate of Income Tax will mean that for the first time, the Welsh Government will have the power to substantially change the size of its budget. The next Welsh Assembly elections, currently scheduled for 2021, may well be fought on competing tax and spend policies. Even without major changes in Welsh tax policy, relative growth in the Welsh tax base will influence the funding available to the Welsh Government, through the operation of the block grant adjustment (BGA) mechanism. [3]

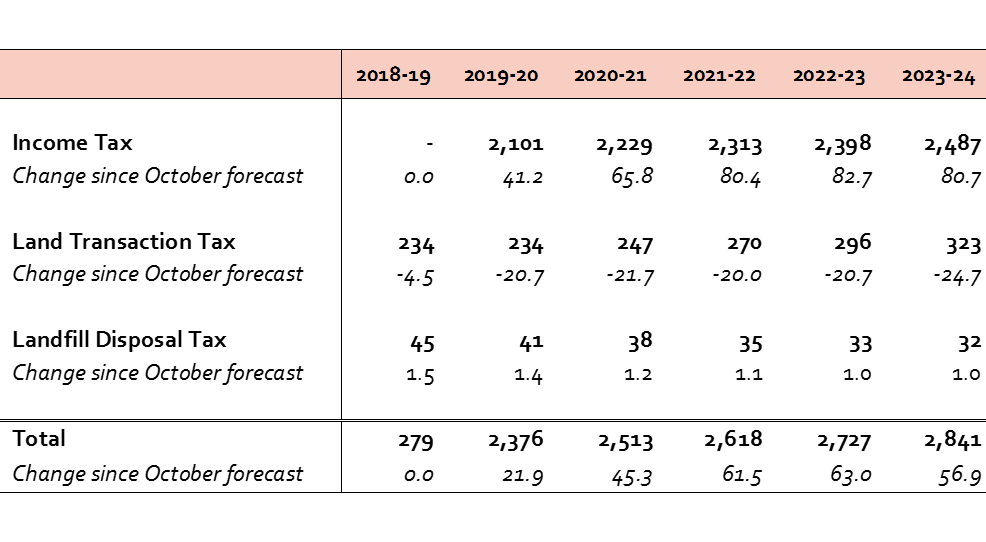

Alongside the Spring Statement, the OBR produced its bi-annual forecasts of devolved taxes. The biggest change since October is an upward revision of projected revenue accruing from devolved Income Tax. Devolved Income Tax revenues are now expected to be higher in each financial year from 2019-20 to 2023-24, resulting in a cumulative increase of £350.8 million by the end of the period compared to previous forecasts.

Increases in Income Tax revenues have been partially offset by a downward revision of forecasted Land Transaction Tax (LTT) revenues.

Compared with previous forecasts, total revenue from devolved taxes is now projected to be £21.9 million higher in 2019-20, £45.3 million higher in 2020-21 and on average £60.5 million higher in each subsequent year until 2023-24 (Figure 3).

Figure 3: Devolved tax revenue forecasts, March 2019 (changes with October 2018 forecasts) £ million

Source: OBR (2018 and previous) Devolved Taxes Forecast March 2019; and authors’ calculations

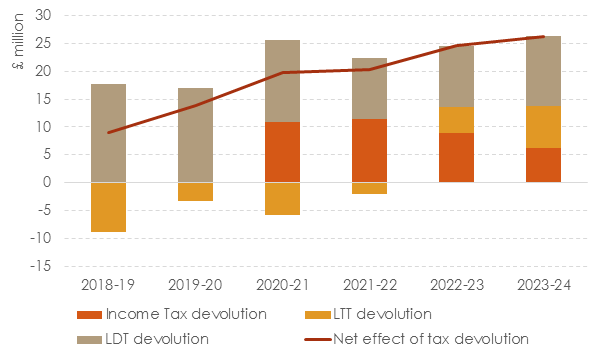

Using forecast revenues for comparable UK government revenues in England and Northern Ireland, we can calculate the net effect of tax devolution compared to a baseline scenario where taxes had not been devolved.

As shown by the red line in Figure 4, the Welsh Treasury is projected to be progressively better off as a result of tax devolution in each year up to the end of the forecast period. Higher forecast Income Tax revenue means that the Welsh budget is projected to be cumulatively better-off by just under £100 million by the end of 2023-24.

Figure 4: Projected net effect of tax devolution, based on March 2019 forecasts

Source: OBR (2018 and previous) Devolved Taxes Forecast March 2019; and authors’ calculations

As well as devolved Income Tax revenues and Non-Domestic rates, Council Tax revenue also funds spending on local public services in Wales.

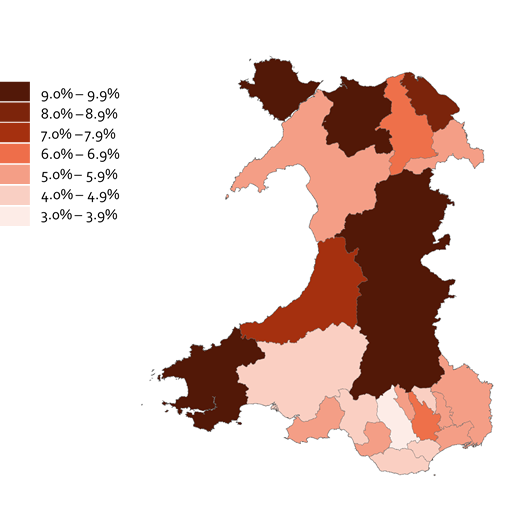

The forecast growth in Council Tax levels for 2019-20 is 4.2%. However, the actual (weighted) average increase for 2019-20 calculated from budgets set by Welsh local authorities over the past month was approximately 6.3%, suggesting that Council Tax growth could well outstrip this forecast (Figure 5).

Figure 5: Percentage increase in Council Tax levels (excl. community and police precepts), 2018-19 to 2019-20

Source: Local Authorities (2019-20) Budgets; and authors’ calculations

Conclusion

Despite slower than expected growth, stronger than expected projections for public finances open the door for sustained increases in public spending over future years. This is in stark contrast with the UK government spending plans laid out in March 2018.

However, as with so much else, the extent to which this increased spending and fiscal certainty materialises depends heavily on what happens to the Brexit process, its economic impact and the potential policy responses.

Notes

[1] The borrowing figure is likely to increase by approximately £12 billion when changes are made to the way student loans are treated on the Government’s books later this year (to reflect that many students will never fully repay their loans).

[2] Several adjustments have been made to the underlying data to produce a consistent series, such as the devolution of Council Tax Benefit and non-domestic rates. Figures are shown before any adjustments for tax devolution from 2018-19.

[3] As a result of tax devolution, a downward adjustment has been made to the Welsh block grant reflecting the revenues being devolved. In future years, this BGA will change according to growth in comparable UK government revenues in England and Northern Ireland. For further details, see Poole et al. (2017).

- September 2024

- July 2024

- June 2024

- December 2023

- November 2023

- August 2023

- February 2023

- December 2022

- November 2022

- September 2022

- July 2022

- April 2022

- March 2022

- January 2022

- October 2021

- July 2021

- May 2021

- March 2021

- January 2021

- November 2020

- October 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- October 2019

- September 2019

- June 2019

- April 2019

- March 2019

- February 2019

- December 2018

- October 2018

- July 2018

- June 2018

- April 2018

- December 2017

- October 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- Bevan and Wales

- Big Data

- Brexit

- British Politics

- Constitution

- Covid-19

- Devolution

- Elections

- EU

- Finance

- Gender

- History

- Housing

- Introduction

- Justice

- Labour Party

- Law

- Local Government

- Media

- National Assembly

- Plaid Cymru

- Prisons

- Rugby

- Senedd

- Theory

- Uncategorized

- Welsh Conservatives

- Welsh Election 2016

- Welsh Elections