Local government finance: the state of play in 2021−22

10 March 2021In what was a bumper week for fiscal events, last week’s headlines were dominated by the UK Budget, which once again extended the vast levels of support for businesses and individuals in the face of ongoing public health restrictions.

A day earlier, the Welsh Government had published its own Final Budget and Local Government Settlement for 2021−22 to significantly less fanfare. No sooner were these documents published than the Welsh Government announced a further large package of non-domestic (business) rates relief for the retail, leisure, and hospitality sector.

With an estimated £1.3 billion of funding to be allocated at future supplementary budgets, and with the prospect of additional in-year consequentials, further spending announcements are expected over the coming months.

This blog post sets the scene for local government as we enter a new financial year and the second year in the shadow of COVID-19.

Final local government settlement 2021-22

The level of core funding included in the final local government settlement remains unchanged since December 2020. Aggregate External Finance – the sum of the hypothecated Revenue Support Grant and Non-domestic rates – will increase by an average of 3.8% in 2021−22, one of the largest increases in recent years. This increase ranges from 2.0% in Ceredigion to 5.6% in Newport.

The Welsh Government opted not to include a funding floor in the final settlement, meaning than any deviation from the average increase reflects differences in the indicator values (and the weighting given to indicators) for each local authority. For instance, in Ceredigion, updated population datasets explain more than 90% of the deviation. Conversely, in Newport, upward revisions of population and pupil population data almost fully account for the higher-than-average uplift to the settlement.

The final settlement does, however, include substantial additional allocations to aid local authorities in their response to COVID-19; £264 million of hypothecated grant funding has been allocated on top of the £13 million previously announced in December.

The bulk of this additional funding (£206.6m), will be delivered through the Single Emergency Hardship Fund. Local authorities will be able to retrospectively submit claims for income lost and additional expenditure incurred because of the pandemic; but unlike this financial year, this fund will only be available as a recourse until the end of September 2021.

For now, this offers reassurance to local authorities that they will continue to be compensated by the Welsh Government for the costs and losses incurred directly because of COVID-19. Given the sustained downward trend in case numbers and early signs of success showed by the vaccine rollout, it is reasonable to assume that many – though by no means all – spending pressures will be alleviated over the coming months.

Other hypothecated funding commitments include £34.4 million to support bus services, £23.3 million for term time Free School Meals, and £11.8 million towards the Accelerated Learning Programme aimed at mitigating gaps in educational attainment that may have arisen because of the pandemic.

The settlement was later supplemented by a £380 million tax relief package for retail, leisure, and hospitality businesses with a rateable value of up to £500,000 for the entirety of the 2021−22 financial year.

This differs to the scheme announced for England in a few key respects. First, the UK government offered 100% relief to retail, leisure, and hospitality premises for the first quarter of 2021−22, and 66% relief for the remaining three quarters. Second, the scheme in England will continue to be available for businesses with a rateable value of over £500,000 (although several large supermarkets and other retailers have repaid the rates relief, handing back an estimated £2bn to the UK Treasury).

A further package of business grant support from the Welsh Government is expected to be announced soon.

Council Tax

Most local authorities have approved their budget plans and set Council Tax levels for 2021−22, with the remainder set to do so over the coming weeks. Based on the budgets that have been approved and those proposed but not yet approved, the county council element of Council Tax will increase by an average of 3.6% in 2021−22.

This represents the smallest increase since 2017, though ahead of inflation. And an average increase of 5.5% to the police precept means that the average increase to bills is likely to be nearer to 4%.

A sharp increase in house prices and a buoyant property market have led some councils to reassess the premiums levied on second homes and long-term empty properties. From April 2021, Gwynedd and Swansea will both levy a 100% premium on second homes, becoming the first local authorities to use the powers to their full extent, netting an additional £6.3 million and £2.9 million, respectively.

Based on current plans, the premium on second homes is estimated to raise nearly £15 million next year, almost double what was raised in 2020−21 and roughly equivalent to a quarter of the revenue generated by higher rate residential property transactions in 2019−20.

A return to austerity?

Despite the additional funding announced for 2021−22 and the lower-than-expected increases to Council Tax levels, the medium-term outlook is much less certain.

The additional grant funding to aid local authorities with their response to COVID-19 has been used almost exclusively to fund new responsibilities and cost pressures that have arisen as a direct result of the pandemic. In many cases, the additional funds have been offset by reduced revenue elsewhere, such as non-domestic rates or income from fees and charges.

And therein lies the challenge for local authorities. The underlying demographic and inflationary pressures – as well as the cracks that have surfaced after a decade of spending cuts – remain.

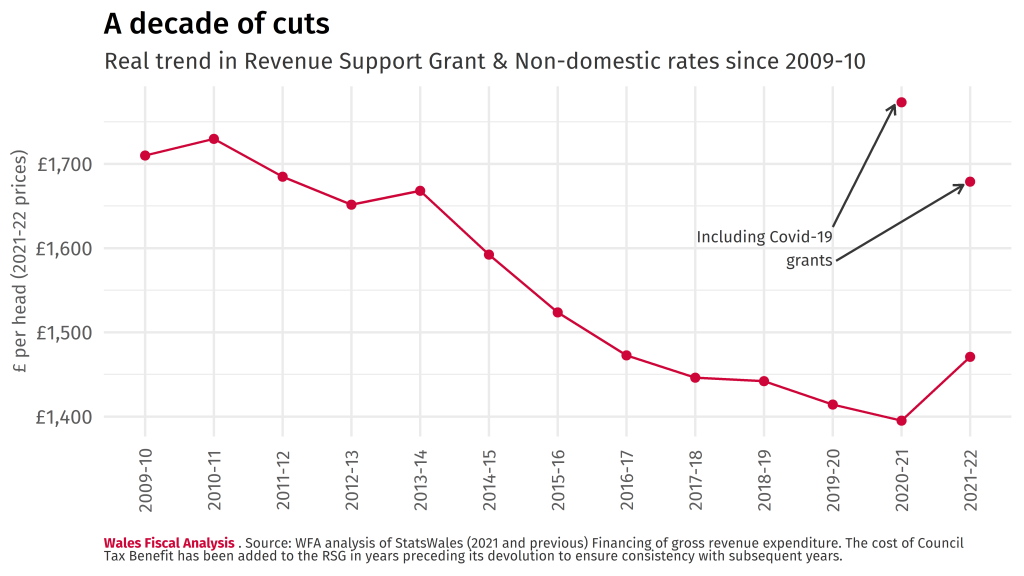

Having adjusted for inflation and population growth, Aggregate External Finance will remain below its 2010−11 level next year − even when COVID-19 grants are included. In their absence, the value of the core settlement is set to be nearly £260 (15%) lower on a per capita basis.

And there is no sign that this trend will be reversed soon.

Based on the spending plans outlined last week, UK government departments outside the NHS, schools, international aid, and defence will see their budgets cut in real terms from 2022−23 onwards. Indeed, if the Chancellor is to reconcile his commitment not to raise Income Tax, National Insurance or VAT rates – which he doubled down on last week – with his aim of realising a current budget balance by 2025-26, this likely implies real terms cuts to some areas of public spending.

The path of the Welsh Budget is still, by and large, determined by changes to the size of the Block Grant. And although the Block Grant is expected to grow over the next five years, in line with comparable spending in England, the most recent spending plans will reduce the projected increase by £600 million compared to the plans set out in March 2020.

The next Welsh Government may find itself in an unenviable position where it must prioritise areas of the budget to protect from spending cuts. And if the local government settlement does not keep up with cost pressures, the burden could once again fall on councils to propose steeper increases to Council Tax, which disproportionately impacts households with lower income levels.

This makes it even more important for us to consider ways of reforming or replacing Council Tax with a more progressive and fairer way of raising revenue locally – a challenge for all political parties ahead of the Senedd election in May.

Wales Fiscal Analysis will be publishing further research on the medium-term fiscal outlook for the Welsh Budget and the likely funding pressures to 2025–26 ahead of the election in May.

Comments

- June 2024

- December 2023

- November 2023

- August 2023

- February 2023

- December 2022

- November 2022

- September 2022

- July 2022

- April 2022

- March 2022

- January 2022

- October 2021

- July 2021

- May 2021

- March 2021

- January 2021

- November 2020

- October 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- October 2019

- September 2019

- June 2019

- April 2019

- March 2019

- February 2019

- December 2018

- October 2018

- July 2018

- June 2018

- April 2018

- December 2017

- October 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- Bevan and Wales

- Big Data

- Brexit

- British Politics

- Constitution

- Covid-19

- Devolution

- Elections

- EU

- Finance

- Gender

- History

- Housing

- Introduction

- Justice

- Labour Party

- Law

- Local Government

- Media

- National Assembly

- Plaid Cymru

- Prisons

- Rugby

- Theory

- Uncategorized

- Welsh Conservatives

- Welsh Election 2016

- Welsh Elections

1 comment

Comments are closed.