Covid-19 and the economic challenges facing the incoming Welsh Government – part 1

14 May 2021In this series of blog posts, Jesús Rodríguez from the Wales Fiscal Analysis (WFA) team explores the economic challenges facing the incoming Welsh Government in recovering from Covid-19

The 2021 Senedd election on 6 May took place amid a significant reduction in Covid-19 cases and deaths. Some restrictions implemented to contain the spread of the virus have been progressively eased by the Welsh Government. The economy had been frozen by the lockdown and social distancing measures since December 2020 and some economic sectors such as non-essential retail, accommodation, transport, and leisure services have been substantially affected by the pandemic.

Economic recovery will be one of the central items on the political agenda facing the Welsh Labour government. This two-part series of blog posts provides an overview of the current economic situation in Wales as measured by a set of short-term output indicators and the latest labour market data. It aims to inform public debate on the current state of the Welsh economy, provide some medium-term projections and assess the economic challenges for the next Senedd term.

Impact of COVID-19 on the Welsh economy

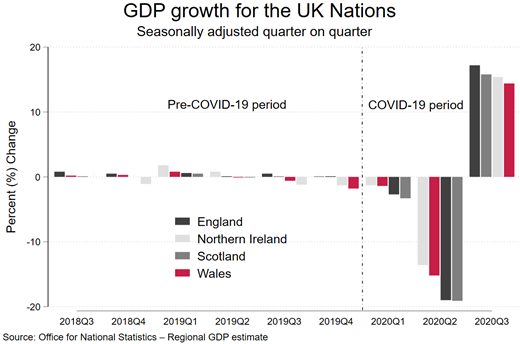

On 5 May, the Office for National Statistics (ONS) released data on the GDP performance for the countries and regions of the UK up to Q3 (July to September) 2020. After a contraction of historical magnitudes in the second quarter of 2020 (-18.8%) as a result of the first national lockdown, the UK GDP showed a significant recovery in Q3 (+16.9%).

Figure 1

As shown in Figure 1, England was the nation that registered the fastest rebound in economic growth, of 17.2% in Q3, followed by Scotland (15.8%), Northern Ireland (15.4%) and Wales (14.4%). Although Wales experienced the smallest rebound, it is worth noting the initial decline in Welsh GDP in the second quarter was lower (at -15.2%) than that registered by the UK (-18.8%).

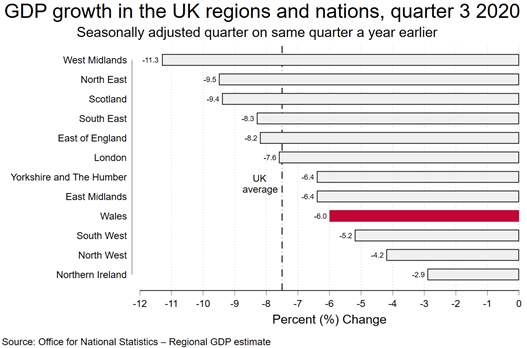

Figure 2 depicts the annual change in GDP in Q3 2020 when compared with the same quarter a year earlier, in each UK nation and region. The West Midlands showed the largest annual fall (-11.3%). In contrast, Northern Ireland showed the smallest annual declines at negative 2.9%. Welsh GDP was 6.0% smaller than the previous year – a smaller decrease than the UK as a whole (7.5%).

Figure 2

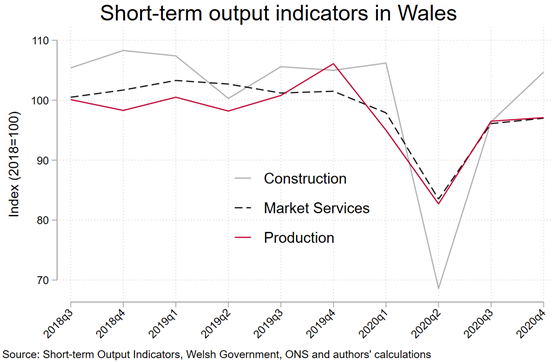

In addition to GDP estimates to Q3 2020, we also have indicators of Welsh output covering the period from October to December 2020, published by the Welsh Government. The estimates consist of a set of short-term indicators in the areas of construction, market services and production. These indices account for 73% of the total Welsh economy and can therefore be used to gauge key trends and short-term movements in the output of companies in these sectors in Wales. [1]

Figure 3 shows the quarterly performance of these sectors of the Welsh economy before and after the pandemic. The unprecedented magnitude of the economic contraction of the last year can be clearly seen. The three indicators fell substantially between February and April 2020 (second quarter) as a result of the first nationwide lockdown and social distancing measures to mitigate the spreading of COVID-19. The largest fall occurred in the construction sector with a decrease rate of -35.3% compared to the previous quarter, followed by market services (-14.8%) and the index of production (-11.7%).

After this enormous negative shock, we see a rapid growth during the summer months as the restrictions eased and the economy opened back up. In the 3rd quarter 2020, the index of market services increased by 15.4% compared to the previous quarter, mostly driven by accommodation and food service activities. Similarly, the index of production − which comprises manufacturing, mining, electricity, and water supply − increased by 15.9%. In addition, compared to the previous quarter, the index of construction increased by 40.5%.

In the 4th quarter 2020, the index of construction again rose by 8.7% and both the index of market services and production grew slightly, at a rate of 0.9% and 0.5%, respectively. Overall, the index of market services decreased by 8.4% on an annual basis, representing the largest fall since the series began. This compared to a fall of 9.8% across the UK.

Figure 3

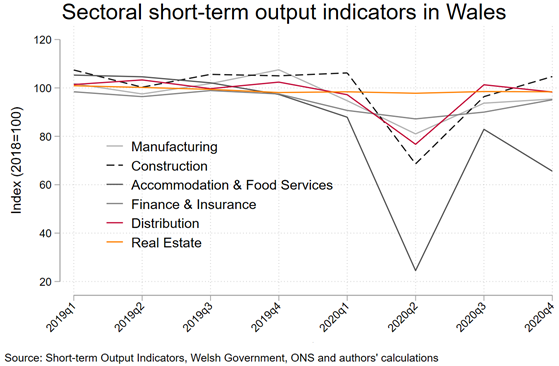

One of the main attributes of this economic crisis has been its unequal impact across different sectors, businesses, and individuals. Service providers that have been able to work remotely, stay open during lockdowns, and/or substitute online for in-person activities have been much less impacted. Firms whose activities require physical proximity and face to face interaction have been more severely affected.

Figure 4 provides a more disaggregated picture from the short-term output indicators, showing the most important and most affected economic sectors. ‘Accommodation & Food Services’, ‘Construction’ and ‘Distribution’ are the sectors that have been more affected by the crisis, while ‘Real Estate’ and ‘Finance & Insurance’ have been less affected given their ability to do much of their business remotely.

This differential impact between sectors points to a “K-shaped” recovery, given the fact some restrictions are likely to continue for some sectors in 2021. It is expected output in industries such as tourism, leisure and hospitality will not have returned to pre-pandemic levels in 2021. This is a challenge the Welsh Government will have to address considering these sectors usually hire more low-income earners, women, and younger workers – the groups more severely affected by lockdowns and with less potential for remote working.

Figure 4

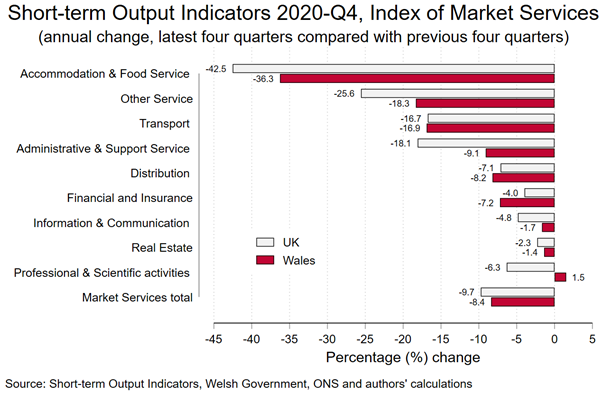

Figure 5

Figure 5 presents the annual change for each sub-index of the ‘Market Services’ sector over 2020 compared to 2019, showing the differential impact on some sectors. While output in Wales decreased by a proportionately greater amount than the UK as a whole in some sectors, some sectors performed somewhat better in Wales, for example, ‘Accommodation & Food Service’, ‘Administrative & Support Service’ and ‘Professional & Scientific activities’. In fact, the latter was the only index showing growth across 2020. This category includes many different professional occupations, and the stronger performance likely signals greater prevalence of homeworking during the pandemic.

Medium-term economic outlook for Wales

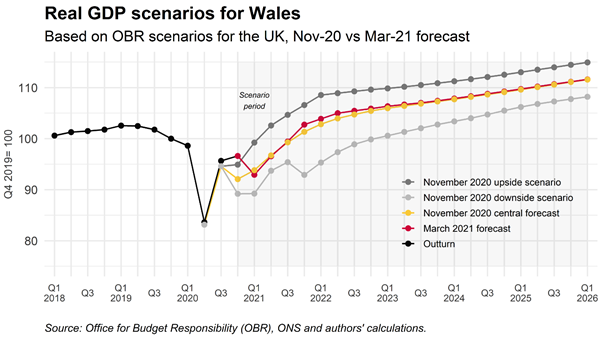

To explore the possible economic outlook for Wales over coming years, we can take the latest OBR economic forecasts for the UK economy and what this may suggest for the Welsh economy. The latest forecasts were published in March 2021, which considered the latest data and government policies to the March 2021 budget. The forecasts assumed the successful rollout of the vaccine and easing of public health restrictions in line with the UK Government’s 22 February roadmap. Consumption and output were expected to rebound through this year driven by release of the extra savings accumulated by households during the pandemic.

Figure 6 shows the path of Welsh GDP if it follows the trends implied by the OBR’s forecasts. We also show the upside and downside scenarios published by the OBR in November 2020. With new restrictions and lockdowns being introduced in the UK due to the emergence of the second wave of Covid-19, the OBR forecast that the UK economy would shrink again by -3.8% in the first quarter of 2021, following the initial recovery. The first quarterly estimate by the ONS for this quarter shows a smaller contraction of 1.5%, meaning output was 8.7% below pre-pandemic levels.

Figure 6

The OBR’s forecast for the UK projected output to reach above pre-pandemic levels by the second quarter of 2022. Since the initial economic fall for Wales was smaller (see Figure 2), in our projections output in Wales would reach pre-pandemic levels by the last quarter of 2021, if growth matches forecast UK trends. Beyond this point, the OBR forecast some ‘scarring effect’ of the pandemic and continue to assume output will be 3 per cent below its pre-pandemic path over the medium-term.

The second part of this series of blogs will explore the latest picture for the Welsh labour market and the challenges facing the next Welsh Government.

Data and replication files for this blog can be found here.

[1] Estimates for Wales are typically more volatile than for the UK and therefore comparisons between Wales and the UK should be treated with caution.

- December 2023

- November 2023

- August 2023

- February 2023

- December 2022

- November 2022

- September 2022

- July 2022

- April 2022

- March 2022

- January 2022

- October 2021

- July 2021

- May 2021

- March 2021

- January 2021

- November 2020

- October 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- October 2019

- September 2019

- June 2019

- April 2019

- March 2019

- February 2019

- December 2018

- October 2018

- July 2018

- June 2018

- April 2018

- December 2017

- October 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- Bevan and Wales

- Big Data

- Brexit

- British Politics

- Constitution

- Covid-19

- Devolution

- Elections

- EU

- Finance

- Gender

- History

- Housing

- Introduction

- Justice

- Labour Party

- Law

- Local Government

- Media

- National Assembly

- Plaid Cymru

- Prisons

- Rugby

- Theory

- Uncategorized

- Welsh Conservatives

- Welsh Election 2016

- Welsh Elections